Welspun Corp Limited (WCL) reported a strong financial performance for FY26, highlighting robust growth across its infrastructure-focused businesses and reinforcing its transition beyond its traditional line pipe operations. The company exceeded its EBITDA guidance for the year and delivered a Return on Capital Employed (ROCE) of 22.3%, reflecting improved operational efficiency and capital discipline.

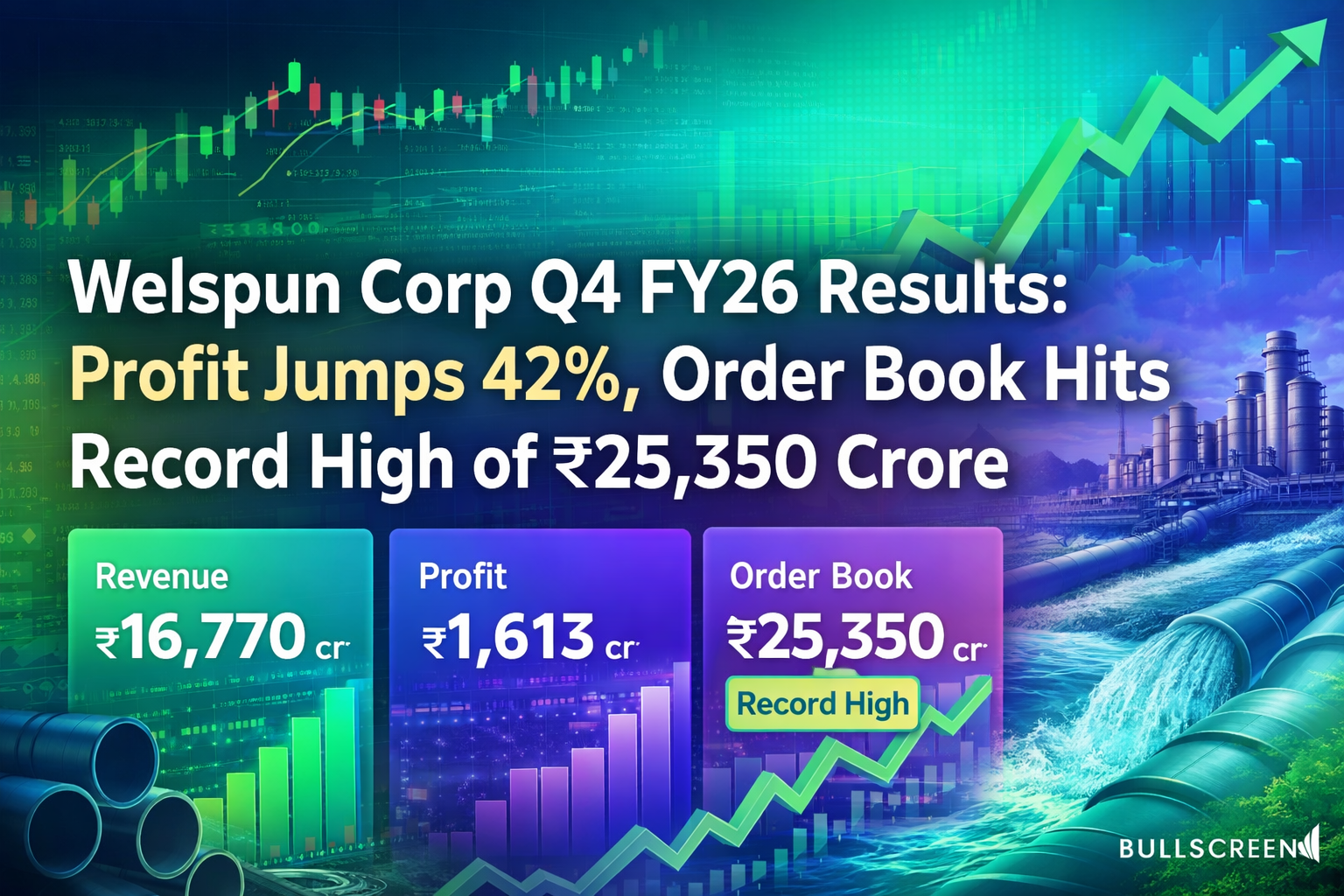

For FY26, consolidated revenue from operations rose 20% year-on-year to ₹16,770 crore, while EBITDA increased 28% to ₹2,371 crore. EBITDA margin improved to 14.0% from 13.1% a year earlier. Profit before tax surged 52% to ₹1,804 crore, while profit after tax, excluding exceptional items, climbed 42% to ₹1,613 crore.

A major highlight was the sharp improvement in cash generation. Operating cash flow more than doubled to ₹3,204 crore from ₹1,504 crore in FY25. Despite capital expenditure of ₹2,532 crore during the year, the company maintained a healthy net cash position of ₹1,627 crore.

Operationally, Welspun Corp recorded growth across key segments. Line pipe sales increased 12% to 954 KMT, supported by strong demand and a fully booked USA spiral mill through FY28. Ductile iron pipe volumes rose 26% to 342 KMT, benefiting from irrigation and water infrastructure projects, while stainless steel bar volumes jumped 44% to 27.2 KMT.

The company’s order book reached an all-time high of ₹25,350 crore, providing strong revenue visibility. Management has guided for FY27 revenue of ₹20,000 crore and EBITDA of ₹2,850 crore, implying another year of double-digit growth.

The board also recommended a dividend of ₹5 per equity share. With improving profitability, strong cash flows, and expanding infrastructure exposure, Welspun Corp appears well-positioned to sustain growth momentum in the coming years.

| Metric | FY25 | FY26 | Growth |

|---|---|---|---|

| Revenue | ₹13,978 Cr | ₹16,770 Cr | ▲ 20% |

| EBITDA | ₹1,858 Cr | ₹2,371 Cr | ▲ 28% |

| EBITDA Margin | 13.1% | 14.0% | ▲ 90 bps |

| Profit Before Tax (PBT) | ₹1,187 Cr | ₹1,804 Cr | ▲ 52% |

| PAT* | ₹1,133 Cr | ₹1,613 Cr | ▲ 42% |

| Operating Cash Flow | ₹1,504 Cr | ₹3,204 Cr | ▲ 113% |

*PAT excluding exceptional items

| Business Segment | FY26 Volume | YoY Growth |

|---|---|---|

| Line Pipes (India + USA) | 954 KMT | ▲ 12% |

| Ductile Iron Pipes | 342 KMT | ▲ 26% |

| Stainless Steel Bars | 27.2 KMT | ▲ 44% |

| Order Book | ₹25,350 Cr | Record High |

| ROCE | 22.3% | Strong Improvement |

| Net Cash Position | ₹1,627 Cr | Healthy Balance Sheet |

| Key Indicator | FY27 Target |

|---|---|

| Revenue Target | ₹20,000 Cr |

| EBITDA Target | ₹2,850 Cr |

| Expected Revenue Growth | ~19% |

| Expected EBITDA Growth | ~20% |

| ROCE Goal | Above 20% |

| Net Debt / EBITDA | Below 1x |

| Dividend Recommended | ₹5 per Share |

Source: https://www.bseindia.com/xml-data/corpfiling/AttachHis/d4972016-6d1e-4eaa-8dd9-210436acf06c.pdf