South West Pinnacle Exploration Limited reported strong growth in its Q4 results 2026 update, supported by higher drilling activity, expansion in mining services, and rising contributions from Coal Bed Methane (CBM) production.

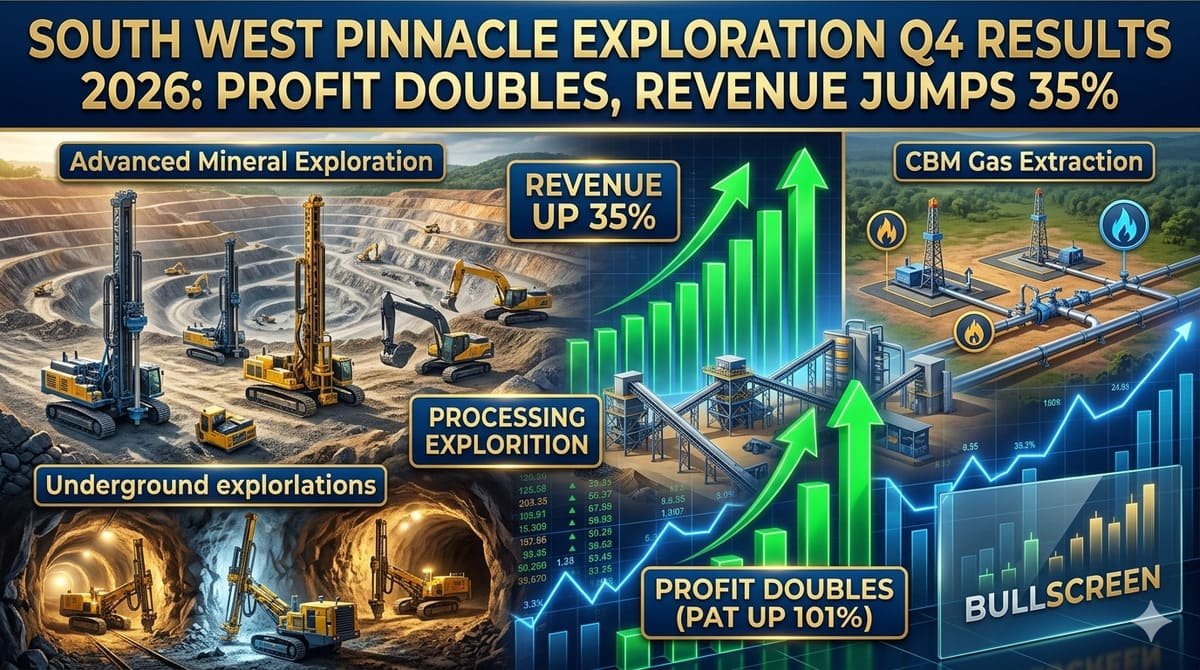

The company posted its highest-ever annual operating revenue of INR 2,430 million for FY26, up 34.8% year-on-year from INR 1,803 million in the previous fiscal. EBITDA climbed 73.5% to INR 583 million, while EBITDA margins improved sharply to 23.99% from 18.64% a year earlier.

Profit after tax more than doubled to INR 330 million, registering 101.2% growth compared to FY25. Diluted earnings per share also rose 85.6% to INR 10.82. The strong earnings performance reflected improved execution across exploration and drilling contracts as well as better operational efficiency.

South West Pinnacle Exploration ended FY26 with an order book of INR 5,812 million, with nearly 73% coming from private sector clients. The “Survey and Exploration of Minerals” segment accounted for the largest share of pending orders, highlighting continued demand from the mining industry.

Operationally, the company crossed 3.2 million meters of cumulative drilling and currently operates 47 hydrostatic drilling rigs across India and overseas markets. CBM production remained the biggest revenue contributor at 37.19%, followed by aquifer mapping and non-coal exploration services.

The company also continued expanding internationally through its Oman joint ventures, including an 11-year USD 125 million copper mining contract. In India, its Jharkhand coal block with 84 million tonnes of reserves is expected to begin production by FY28.

With improving return ratios, a debt-to-equity ratio of 0.39, and expanding mining exposure, investors will closely track how the company sustains growth momentum after its strong Q4 results 2026 performance.

| Metric | FY26 Performance | YoY Growth |

|---|---|---|

| Revenue from Operations | INR 2,430 Mn | +34.8% |

| EBITDA | INR 583 Mn | +73.5% |

| EBITDA Margin | 23.99% | +535 bps |

| Profit After Tax (PAT) | INR 330 Mn | +101.2% |

| Diluted EPS | INR 10.82 | +85.6% |

| ROE | 16% | vs 10% in FY25 |

| ROCE | 23% | vs 16% in FY25 |

| Debt-to-Equity Ratio | 0.39 | Stable |

| Metric | Details |

|---|---|

| Order Book | INR 5,812 Mn |

| Private Sector Share | 73% of total order book |

| Largest Segment | Survey & Exploration of Minerals |

| Total Drilling Achieved | 3.2+ Million Meters |

| Drilling Rig Fleet | 47 Hydrostatic Rigs |

| Safety Record | Zero Lost Time Injuries Since Inception |

| Largest Revenue Contributor | CBM Production (37.19%) |

| Market Cap (March 2026) | INR 6,309.05 Mn |

| Metric | Key Updates |

|---|---|

| Oman Mining JV | USD 125 Million Copper Mining Contract |

| Oman Block 22-B | Copper, Gold & Silver Reserves |

| Jharkhand Coal Block | 84 Million Tonnes Geological Reserves |

| Coal Production Target | FY 2027-28 |

| International Investment | AUD 0.5 Million in Alara Resources Ltd |

| 52-Week Stock Range | INR 242.55 / 101.05 |

| Current Market Price (CMP) | INR 211.50 |

Source: https://www.bseindia.com/xml-data/corpfiling/AttachHis/e8058501-b827-47e4-a0ac-a865cd24db67.pdf