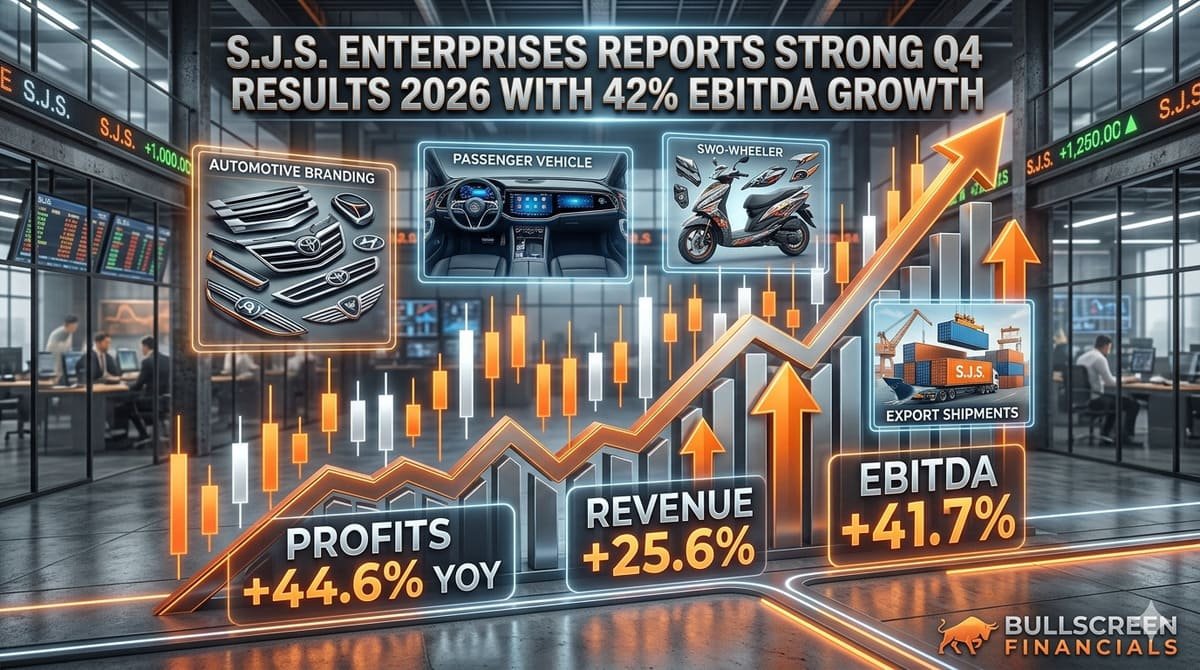

S.J.S. Enterprises Limited reported its strongest-ever quarterly and annual performance in its Q4 results 2026, driven by robust demand from the two-wheeler and passenger vehicle segments, rising exports, and improving margins.

The company posted record quarterly revenue of Rs. 2,601.2 million in Q4 FY26, up 29.7% year-on-year. Growth was led by a sharp 41.1% rise in the two-wheeler segment and a 40.9% increase in passenger vehicle-related business. Export revenue also jumped 74.6% YoY to Rs. 255.5 million during the quarter, highlighting growing overseas traction.

For the full fiscal year, operating revenue rose 25.6% to Rs. 9,550.7 million compared to Rs. 7,604.9 million in FY25. EBITDA climbed 41.7% to Rs. 2,879.6 million, while EBITDA margin expanded 320 basis points to 29.6%. Profit after tax increased 44.6% to Rs. 1,718 million, with PAT margin improving to 18%.

The company continued to outperform the broader automobile industry. While the combined two-wheeler and passenger vehicle industry grew 11.4% in FY26, S.J.S. Enterprises recorded 35% growth, marking its 26th consecutive quarter of industry outperformance.

The company also strengthened its balance sheet with a net cash position of Rs. 2,437.1 million and improved return ratios. ROCE rose to 35.5%, while ROE increased to 19.5% during FY26. ICRA upgraded its long-term credit rating to AA- (Positive).

During the year, the company expanded manufacturing capabilities and signed a technology partnership with BOE Varitronix to assemble automotive displays in India. It also secured new business from major OEMs including Tata Motors, Hyundai, Mahindra, and Samsung.

The board declared a final dividend payout of 35% of face value following the strong Q4 results 2026 performance.

| Metric | FY26 | FY25 | YoY Growth |

|---|---|---|---|

| Operating Revenue | Rs. 9,550.7 Mn | Rs. 7,604.9 Mn | +25.6% |

| EBITDA | Rs. 2,879.6 Mn | Rs. 2,032.1 Mn | +41.7% |

| EBITDA Margin | 29.6% | 26.4% | +320 bps |

| Profit After Tax (PAT) | Rs. 1,718 Mn | Rs. 1,188.4 Mn | +44.6% |

| PAT Margin | 18.0% | 15.6% | +240 bps |

| EPS | Rs. 54.02 | Rs. 37.82 | +42.8% |

| Metric | Performance |

|---|---|

| Highest Quarterly Revenue | Rs. 2,601.2 Mn |

| Q4 Revenue Growth | +29.7% YoY |

| 2W Segment Growth | +41.1% YoY |

| Passenger Vehicle Growth | +40.9% YoY |

| Export Revenue Growth | +74.6% YoY |

| Final Dividend | 35% payout of face value |

| Industry Growth vs SJS Growth | 11.4% vs 35.0% |

| Consecutive Industry Outperformance | 26 Quarters |

| Metric | FY26 Update |

|---|---|

| Net Cash Position | Rs. 2,437.1 Mn |

| ROCE | 35.5% |

| ROE | 19.5% |

| Export Contribution | 9.5% of Revenue |

| New Generation Products Contribution | 24% of Revenue |

| Credit Rating Upgrade | ICRA AA- (Positive) |

| New Facility | Hosur plant under construction |

| Key OEM Customers | Tata Motors, Hyundai, Mahindra, Samsung |

| Technology Partnership | BOE Varitronix automotive displays |

Source: https://www.bseindia.com/xml-data/corpfiling/AttachHis/3ae96367-c266-459a-833e-885274172388.pdf