Madhya Bharat Agro Products Limited reported a strong set of Q4 results 2026, capping a record financial year with sharp growth in revenue, profit, and operational performance.

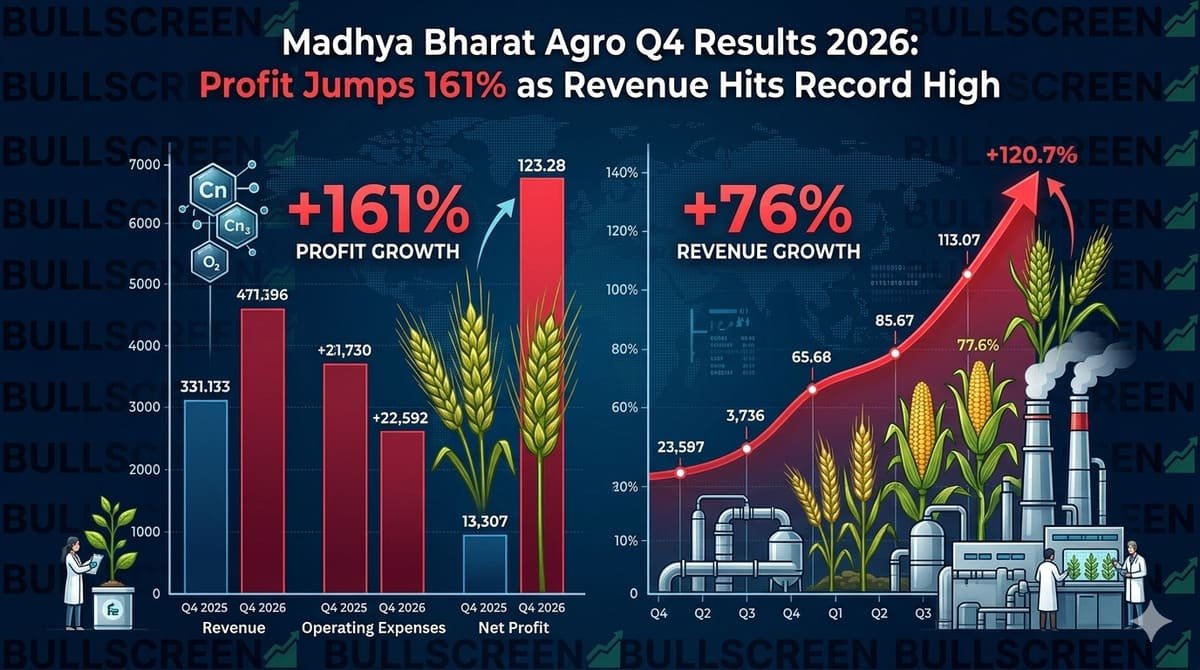

The company posted revenue from operations of ₹1,867 crore for FY26, marking a robust 76% year-on-year rise. Profit after tax surged 161% to ₹150.2 crore, while earnings per share climbed to a record ₹17.14 from ₹6.56 in the previous year. EBITDA stood at ₹226.5 crore with a margin of 12.1%, compared to ₹145.4 crore in FY25, highlighting improved operational efficiency.

The Q4 results 2026 reflect strong execution and rising demand in the fertilizer sector. Return on equity more than doubled to 31.51%, underlining efficient capital utilization. Additionally, the company’s credit rating was upgraded to A+/Stable by both CRISIL and ICRA, indicating improved financial strength.

Operationally, the company achieved record production of 475,154 metric tonnes and sales of 472,270 metric tonnes during FY26. Capacity utilization remained high, with NPK/DAP plants operating above 100% and SSP plants at 98%. The company now holds around 9% market share in India’s SSP segment, reinforcing its position among leading phosphatic fertilizer producers.

A key driver behind the performance in the Q4 results 2026 is its backward integration model. With in-house capabilities across rock phosphate beneficiation, sulphuric acid, and phosphoric acid production, the company has been able to secure raw materials efficiently and maintain cost advantages.

Strategic expansions also played a major role. New capacities at Dhule and Sagar are expected to significantly enhance output, with management indicating potential revenue addition of nearly ₹3,500 crore at full utilization.

In a major development, the company secured India’s largest long-term green ammonia supply deal under the National Green Hydrogen Mission. The agreement ensures supply at nearly ₹53 per kg, substantially lower than global benchmarks, improving cost competitiveness while supporting sustainability goals.

Looking ahead, the company plans to further expand capacities by FY28, aiming to capitalize on rising demand for balanced fertilization and food security. The strong Q4 results 2026 signal sustained growth momentum and improving industry positioning.

| Category | Metric | FY26 Performance | Growth / Change |

|---|---|---|---|

| Financial Performance | Revenue from Operations | ₹1,867 crore | 🔼 +76% YoY |

| Profit After Tax (PAT) | ₹150.2 crore | 🔼 +161% YoY | |

| EBITDA | ₹226.5 crore | 🔼 +56% YoY | |

| EBITDA Margin | 12.1% | Slight decline | |

| Earnings Per Share (EPS) | ₹17.14 | 🔼 Strong growth | |

| Return on Equity (ROE) | 31.51% | 🔼 Significant jump | |

| Operational Metrics | Total Production | 475,154 MT | Record High |

| Total Sales | 472,270 MT | Record High | |

| NPK/DAP Utilization | 100%+ | Peak efficiency | |

| SSP Utilization | 98% | Near full capacity | |

| SSP Market Share | 9% | मजबूत presence | |

| Capacity & Expansion | Dhule Expansion (SSP) | +330,000 MTPA | New capacity added |

| Dhule Sulphuric Acid | +198,000 MTPA | Expansion | |

| Sagar NPK/DAP Capacity | 330,000 MTPA | 🔼 +38% | |

| Sagar Sulphuric Acid | 330,000 MTPA | 🔼 Doubled | |

| Revenue Potential from Expansion | ₹3,500 crore | Future upside | |

| Strategic Highlights | Green Ammonia Deal | 130,000 MTPA (10 yrs) | Largest in India |

| Ammonia Cost | ₹53/kg | 🔽 Lower cost | |

| Sustainability Push | Under National Green Hydrogen Mission | ESG aligned | |

| Credit & Strength | Credit Rating | A+/Stable | Upgraded by CRISIL & ICRA |

| Future Outlook | NPK/DAP Capacity Target (FY28) | 990,000 MT | Expansion planned |

| Phosphoric Acid Target | 165,000 MT | Growth pipeline |

Source: https://nsearchives.nseindia.com/corporate/MBAPL_18042026103333_MBAPL.pdf