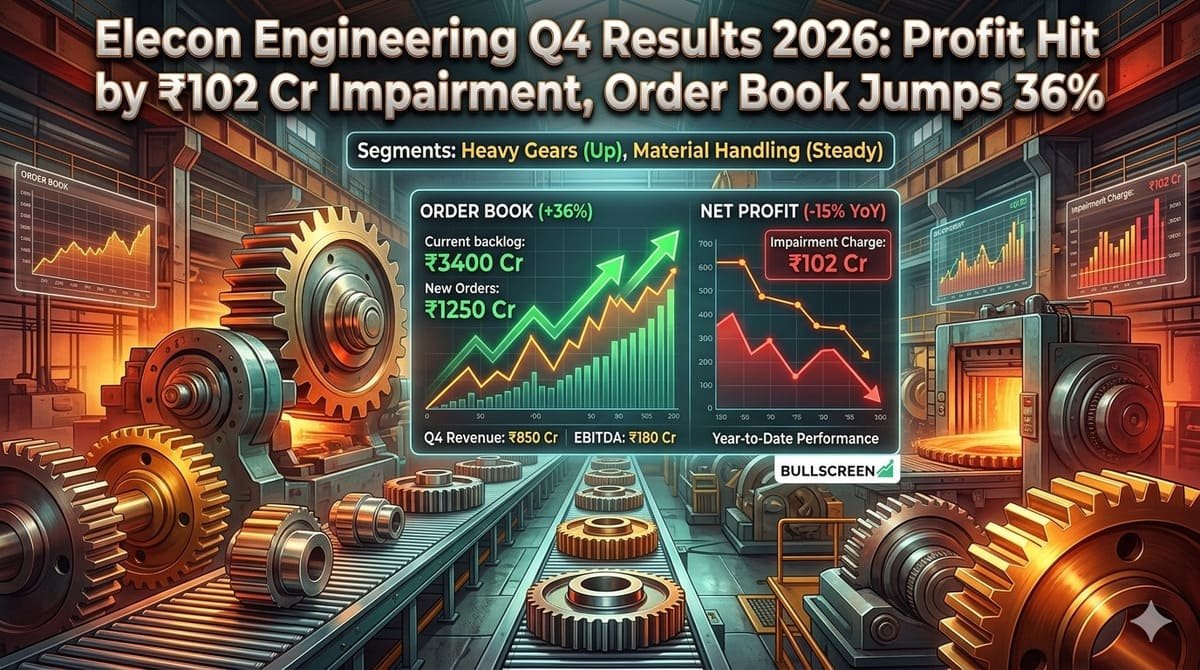

Elecon Engineering Company Limited reported a mixed set of Q4 results 2026, with a sharp one-time impairment dragging profits even as its order book and core operations showed resilience.

For the full year FY26, the company posted consolidated revenue of ₹2,366 crore, marking a 6% year-on-year rise. EBITDA came in at ₹523 crore with a margin of 22.1%, supported partly by a one-time arbitration income of ₹25 crore. Profit after tax stood at ₹341 crore, translating to a margin of 14.4%.

However, the headline numbers for Q4 results 2026 were impacted by a ₹102 crore goodwill impairment, a non-cash exceptional item that weighed on quarterly profitability.

A key highlight was the company’s strong order momentum. The total order book rose 36% year-on-year to ₹1,292 crore as of March 31, 2026, signaling healthy demand visibility going into FY27.

The Gear division, traditionally the company’s mainstay, faced pressure during the quarter. FY26 revenue from the segment declined 3.6% to ₹1,699 crore, while Q4 revenue dropped sharply by 21% due to customer deferments and delayed dispatches. Despite this, order intake remained strong, with the division’s order book rising 53.3% to ₹894 crore.

In contrast, the Material Handling Equipment (MHE) division emerged as the growth engine. Revenue surged 43.6% year-on-year to ₹667 crore, driven by strong execution and expansion in after-sales services. The division maintained a healthy EBIT margin of 22.8% in Q4, cushioning the overall performance.

Operational ratios remained stable, though slightly softened compared to last year. The company continued to maintain a net cash position with a low debt-to-equity ratio of 0.12x.

Key Financial Snapshot (FY26)

| Metric | FY26 | FY25 |

|---|---|---|

| Revenue | ₹2,366 Cr | ₹2,227 Cr |

| EBITDA | ₹523 Cr | — |

| PAT | ₹341 Cr | — |

| RoNW | 15.9% | 21.0% |

| RoCE | 20.4% | 26.8% |

| Order Book | ₹1,292 Cr | ₹950 Cr (approx) |

Despite near-term challenges in Q4 results 2026, the company’s expanding global footprint across 95+ countries, strong manufacturing base, and growing MHE business provide long-term stability.

The sharp rise in order book and improving segment mix indicate that Elecon Engineering may be positioning for a stronger recovery in FY27, even as cyclical pressures persist in its core gear business.

Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/87d562c0-fdb5-4776-88ad-7d339e124b94.pdf