Antelopus Selan Energy Limited has reported a strong financial performance for the fiscal year ended March 31, 2026 (FY26), driven by improved operational efficiency, strategic consolidation, and disciplined cost management. The company’s audited results reflect robust profitability growth following its merger with Antelopus Energy Private Limited.

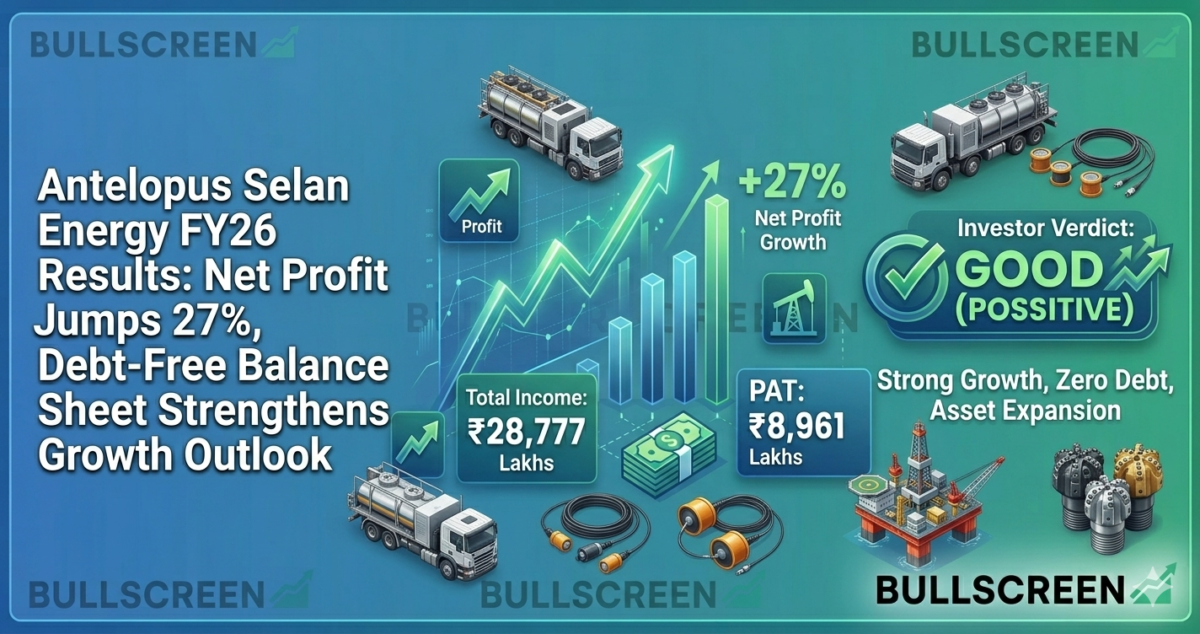

The company posted Total Income of ₹28,777 lakhs, marking a 7.6% year-on-year (YoY) growth, while Net Revenue from Operations rose 8.1% YoY to ₹27,888 lakhs.

More importantly, Net Profit (PAT) surged 27% to ₹8,961 lakhs, compared to ₹7,057 lakhs in the previous year, highlighting a sharp improvement in margins. Earnings per share (EPS) also climbed to ₹25.49, reflecting enhanced shareholder value.

Profit before tax (PBT) grew significantly by 25.9% to ₹11,944 lakhs, even as total expenses declined by 2.5%, underscoring the company’s strong cost control measures.

A key highlight of FY26 results is the company’s ability to expand profitability faster than revenue growth. This was primarily achieved through:

- Reduction in amortization expenses, following a revision in the useful life of oil and gas assets, resulting in savings of ₹1,776 lakhs

- Lower royalty and cess payments, which declined sharply to ₹4,406 lakhs from ₹5,489 lakhs

- Tighter cost management, leading to an overall reduction in total expenses

These factors significantly boosted operating margins and overall financial performance.

Antelopus Selan Energy continues to maintain a debt-free balance sheet, positioning itself as a financially stable and low-risk player in the oil and gas sector.

| Metric | FY26 Value (₹ Lakhs) | FY25 Value (₹ Lakhs) |

|---|---|---|

| Total Assets | 82,409 | 67,102 |

| Oil & Gas Assets (PPE) | 34,034 | — |

| Cash & Bank Balance | 5,214 | — |

| Debt Status | Zero Debt | Zero Debt |

The absence of long-term borrowings provides the company with flexibility to fund future expansion without financial strain.

Antelopus Selan Energy Limited is significantly ramping up investments to enhance its future production capabilities, highlighting a clear long-term growth strategy.

The company’s Capital Work-in-Progress (CWIP) has surged to ₹21,026 lakhs, reflecting a strong pipeline of upcoming infrastructure and production projects. This sharp increase indicates that multiple assets are under development and are expected to contribute to output in the coming years.

In addition, the company has strengthened its presence in the Cambay oil field, investing ₹3,048 lakhs to acquire a 50% stake, along with an additional ₹2,667 lakhs committed under a carry clause for future development expenditure.

Overall, this elevated capital expenditure underscores the company’s strategic focus on scaling operations and expanding its footprint in India’s upstream oil and gas sector, positioning it for sustained production growth and long-term value creation.

Despite delivering strong financial performance in FY26, Antelopus Selan Energy Limited investors should carefully evaluate certain risk factors that could impact future earnings:

A notable portion of the company’s profit growth is accounting-driven, primarily due to lower amortization expenses following a revision in asset life. While this boosts reported earnings, it may not fully reflect underlying operational growth.

The company also reported a ₹472.54 lakh write-off with an unexecuted acquisition deal for the Cambay oil field, highlighting execution risks in expansion strategies.

Additionally, the company’s earnings remain highly sensitive to global crude oil prices and USD/INR exchange rate fluctuations, which can significantly influence revenue realization and profit margins in the oil & gas sector.

Overall, the outlook remains positive, but investors should stay cautious about commodity price volatility, forex risks, and accounting-driven earnings impact, making this stock suitable for those with a balanced risk appetite looking at India’s upstream energy sector growth story.

Source : https://antelopusenergy.com/wp-content/uploads/2026/05/Audited-results.pdf