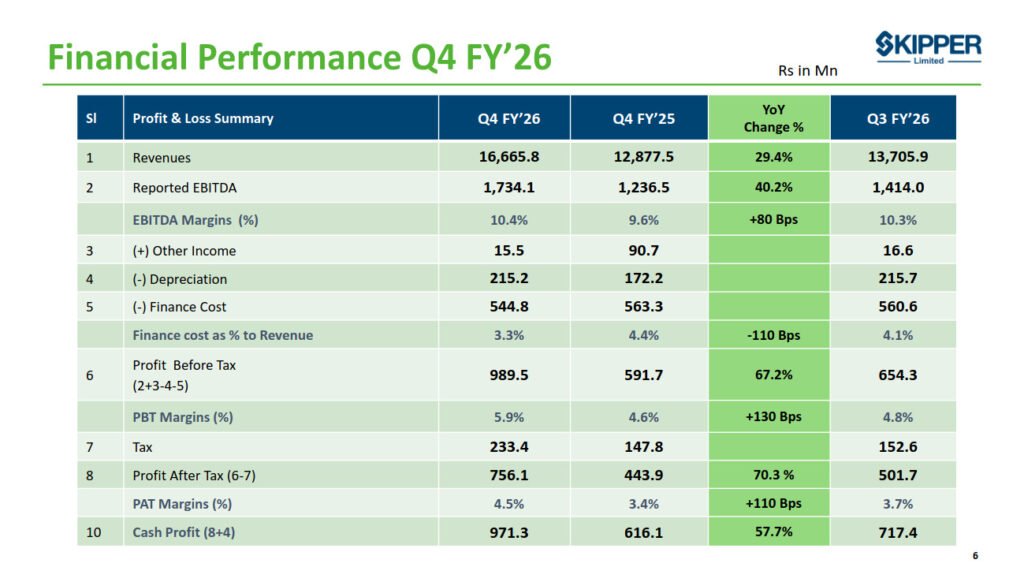

Skipper Limited reported a strong set of Q4 results 2026, capping off a record-breaking financial year with its highest-ever revenue, EBITDA, and profit after tax. The company’s performance was driven by robust execution across segments and a sharp rise in its order book, reinforcing its position in the power transmission and infrastructure space.

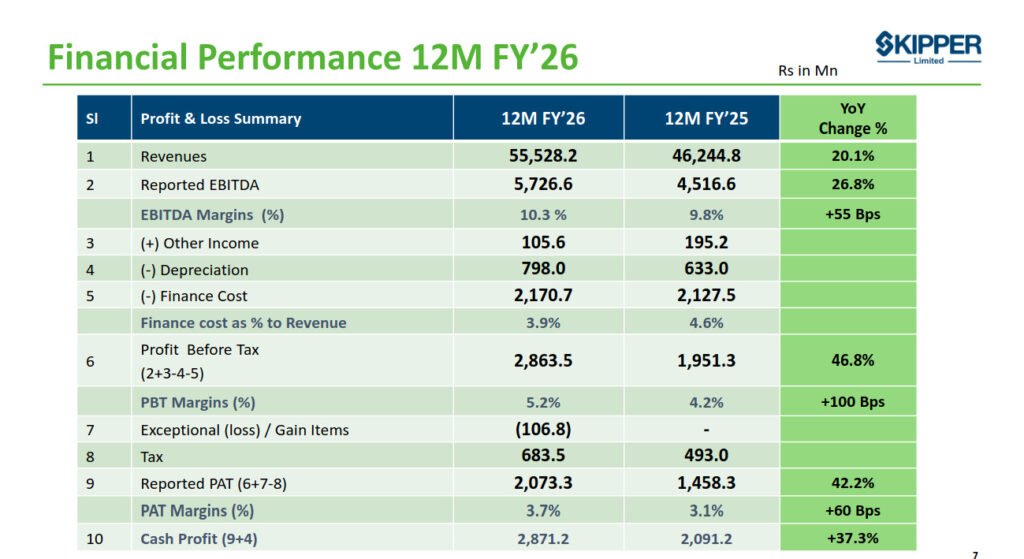

For the full year ending March 31, 2026, revenue rose 20.1% year-on-year to ₹55,528.2 million, compared to ₹46,244.8 million in FY25. EBITDA increased 26.8% to ₹5,726.6 million, with margins improving to 10.3%. Profit after tax surged 42.2% to ₹2,073.3 million, reflecting strong operational efficiency and margin expansion. These Q4 results 2026 also showed improvement in return ratios, with ROE rising to 14.1% from 12.3% a year ago.

Segment-wise, the engineering business remained the primary growth driver, contributing 79% of total revenue at ₹43,590.2 million, up 23.9% YoY. The segment benefited from record volumes and key project wins, including the 800 KV Khavda HVDC project. The polymer segment crossed ₹5,000 million in annual revenue for the first time, growing 17.4%, while infrastructure saw modest growth of 1.9%.

Operationally, the company closed FY26 with a record order book of ₹85,019 million, providing strong revenue visibility. Domestic transmission and distribution accounted for 77% of the order book, followed by exports and non-T&D segments. New order inflows during the year exceeded ₹56,780 million, while the bidding pipeline remained strong at over ₹33,000 million.

Skipper also made strategic progress with capacity expansion plans, aiming to reach 450,000 MTPA by June 2026. Its global footprint expanded with a new subsidiary in Brazil and ongoing setups in the UAE and the US. Technological advancements, including dual tower test bed facilities, further strengthen its competitive edge.

With India’s transmission sector expected to see investments of ₹7.9 lakh crore through 2035-36, Skipper appears well-positioned to benefit from long-term demand driven by renewable energy integration and grid modernization. The strong Q4 results 2026 underline the company’s growth momentum and execution capability.

Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/3693ab1b-835f-47b7-b95e-d6478145fc4d.pdf