Oriental Hotels Limited (OHL) delivered a strong financial performance for FY ended March 31, 2026, marked by double-digit revenue growth, a sharp rise in profitability, improved margins, and continued balance sheet strengthening. The company’s results highlight a clear trend of operational efficiency, deleveraging, and steady hospitality sector recovery.

The company reported robust growth across all key financial metrics, driven by strong hospitality demand and improved operational efficiency.

| Financial Metric | FY 2025-26 | FY 2024-25 | YoY Growth |

|---|---|---|---|

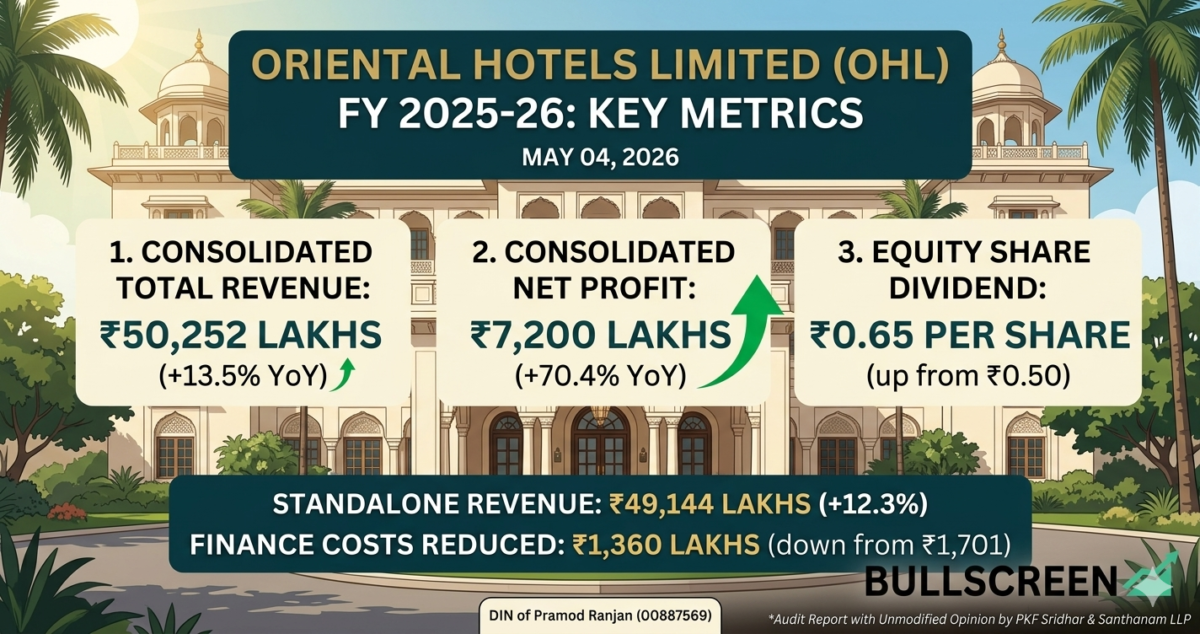

| Total Revenue | ₹50,252 lakhs | ₹44,290 lakhs | +13.5% |

| Net Profit | ₹7,200 lakhs | ₹4,224 lakhs | +70.4% |

| Profit After Tax (including JV/associates) | ₹6,795 lakhs | ₹3,921 lakhs | Strong growth |

| Earnings Per Share (EPS) | ₹3.80 | ₹2.20 | Significant expansion |

The results reflect strong demand in hospitality operations and improved cost control, driving significant profitability expansion.

| Key Metric (₹ Lakhs) | FY 2025-26 | FY 2024-25 | Growth |

|---|---|---|---|

| Revenue from Operations | 49,144 | 43,762 | +12.3% |

| Other Income | 922 | 701 | +31.5% |

| Profit Before Tax | 9,095 | 6,544 | +39.0% |

| Net Profit | 7,077 | 4,452 | +59.0% |

Oriental Hotels significantly strengthened its financial position in FY26, supported by strong cash flow generation and a focused deleveraging strategy.

Debt Reduction

Non-current borrowings reduced to ₹3,742 lakhs from ₹6,090 lakhs

Total Equity

Standalone: ₹48,046 lakhs

Consolidated: ₹76,206 lakhs

Operating Cash Flow

₹12,753 lakhs indicating strong liquidity generation

Investments in Financial Assets

Increased to ₹28,734 lakhs

The company continues a clear deleveraging strategy backed by strong cash flow support.

🔹 TAL Lanka Hotels (Sri Lanka JV)

- Loss narrowed significantly to ₹282 lakhs from ₹531 lakhs

- Investment value stood at ₹5,076 lakhs

Reflects a steady recovery in international hospitality operations

🔹 Jointly Controlled Entity

- Profit share improved to ₹161 lakhs, up from ₹152 lakhs

🔹 Subsidiary Contribution

- Revenue contribution: ₹1,146 lakhs

- Total assets: ₹2,689 lakhs

✔ Strong Revenue Momentum

Sustained recovery in the hospitality sector continues to drive consistent topline growth.

✔ Robust Profit Expansion

Profit surged ~70%, supported by operational efficiency and disciplined cost management.

✔ Deleveraging in Focus

Declining finance costs highlight a stronger balance sheet and reduced debt levels.

✔ Enhanced Shareholder Returns

Higher dividend payout signals confidence in cash flow stability and future earnings visibility.

✔ Improving Operating Leverage

Revenue growth outpacing expenses indicates margin expansion and better profitability outlook.

Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/44744280-2c13-4369-be1f-3cafbbb18cb6.pdf