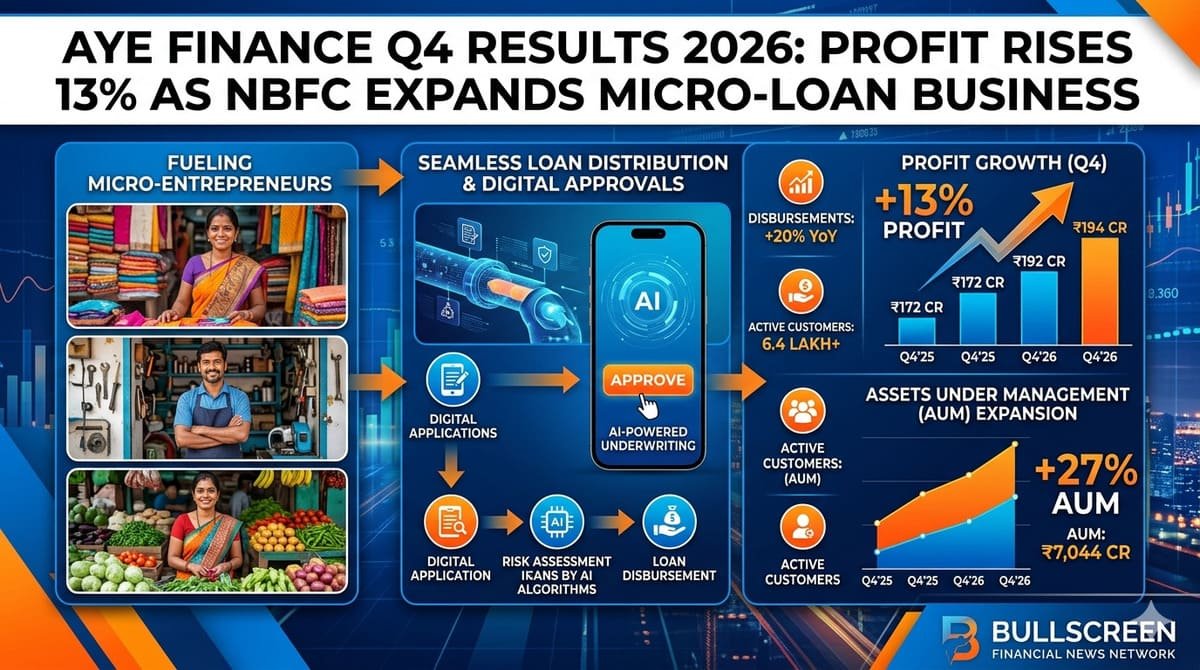

Aye Finance Limited reported a steady financial performance in its Q4 results 2026, capping a year marked by strong growth following its February IPO. The micro-enterprise-focused lender posted a Profit After Tax of ₹194 crore for FY26, up 13% year-on-year, reflecting stable earnings momentum and improved operational efficiency.

Gross total income rose 20% to ₹1,797 crore, driven largely by interest income of ₹1,567 crore, while fee and other income contributed ₹230 crore. The company maintained a healthy Net Interest Margin of 14.64% on average total assets, highlighting its ability to sustain lending spreads despite a competitive credit environment.

Operational metrics showed gradual improvement. The cost-to-income ratio declined to 50.2% from 51.4% a year earlier, supported by controlled expenses of ₹679 crore. Return ratios remained stable, with Return on Assets at 2.8% and Return on Equity at 9.3%, adjusted for fresh capital raised during the IPO.

The company’s asset base expanded significantly, with Assets Under Management growing 27.3% year-on-year to ₹7,044 crore. Annual disbursements rose 20% to ₹5,169 crore, while its active customer base reached approximately 6.4 lakh. Notably, 71% of AUM growth came from existing branches, indicating strong organic expansion rather than aggressive branch additions.

Asset quality improved during the quarter, a key highlight of the Q4 results 2026. Gross NPA declined to 4.77%, while Net NPA stood at 1.8%. Collection efficiency reached 99.5% in March, signaling tighter credit monitoring and recovery processes. The company maintained a Provision Coverage Ratio of 63.66% on stressed assets.

Funding remains diversified across banks, financial institutions, and development lenders. The cost of borrowing eased to 10.13% in Q4FY26, while capital adequacy remained strong at 34.9%, providing room for future growth.

Aye Finance’s “phygital” strategy combining a 571-branch network with AI and machine learning underwriting continues to drive scale. Around 32% of underwriting is now automated, and all loan originations are paperless, improving efficiency and turnaround time.

The Q4 results 2026 underline the company’s focus on disciplined growth, improved asset quality, and technology-led lending. As credit demand from micro-enterprises remains strong, Aye Finance appears well-positioned to expand further while maintaining risk controls.

| Metric | FY26 Value | YoY Growth |

|---|---|---|

| Profit After Tax (PAT) | ₹194 Crores | +13% |

| Gross Total Income | ₹1,797 Crores | +20% |

| Interest Income | ₹1,567 Crores | — |

| Fee & Other Income | ₹230 Crores | — |

| Net Interest Margin | 14.64% | — |

| Cost-to-Income Ratio | 50.2% | Improved |

| Operating Expenses | ₹679 Crores | — |

| Return on Assets (RoA) | 2.8% | — |

| Return on Equity (RoE) | 9.3% | — |

| Metric | FY26 Performance | YoY Growth |

|---|---|---|

| Assets Under Management | ₹7,044 Crores | +27.3% |

| Annual Disbursements | ₹5,169 Crores | +20% |

| Active Customers | ~6.4 Lakh | — |

| Average Ticket Size | ₹1.8 Lakhs | — |

| Net Worth (Equity) | ₹2,533 Crores | ~+53% |

| Branch Network | 571 Branches | — |

| AUM Growth from Existing Branches | 71% | — |

| Metric | Value (FY26 / Q4FY26) |

|---|---|

| Gross NPA (GNPA) | 4.77% |

| Net NPA (NNPA) | 1.8% |

| Portfolio at Risk (PAR X) | 6.88% |

| PAR 30 | 6.1% |

| Collection Efficiency | 99.5% |

| Provision Coverage Ratio (PCR) | 63.66% |

| Total ECL Provisions | ₹267 Crores |

| Cost of Borrowing (Q4FY26) | 10.13% |

| Capital Adequacy (CRAR) | 34.9% |

| AI/ML Underwriting Share | 32% |

| Paperless Loan Origination | 100% |

Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/bad0319d-aa9e-4aa7-bdcb-cdb6debf0a86.pdf